Friends, here’s my post as a part of Value Investing series. Hope you all like it and I shall start the same with my views on one of my favorite favorites – NVIDIA Corporation.

Disclaimer: I’m not any registered stock market broker/trader/analyst. All views are personal and I shall essentially talk about the Company, its vitals, what underscores the selection for me. I will also touch a little about Valuation.

NVIDIA Corporation (ticker symbol: NVDA):

Why NVIDIA?

The reason for me to invest in this Company?

Well, when I was growing up in 2000s, there were very few Global Technology Companies in India we knew of which included the names like AMD, Intel, Microsoft, IBM, Linux, HP and NVIDIA. Today, we are in 2020 and these names have become bolder, stronger and popular. After having started my investing journey in Indian equities in 2006, it was time for me to include a tadka of global giants never tasted before!!!

For some good reason, global brands fascinated us when we were kids. Always felt proud having NVidia operated Computer to using a razor from the stable of Gillette Company. But then soon I realized, wouldn’t it be a lot better to be an owner in such firms than to be a consumer only. One may think that having a fetish for one particular product or a brand do not give a holistic picture about the Company as a whole. Well, I agree, any investment needs to be supported by a deep analysis, however, the starting point for me to think about this one particular company was: if this Company could go past all headwinds and through different economic cycles, then there isn’t much for me to look into as an investment over a long term; and potentially the maximum I could lose is the capital, but in the process I would end up learning a lot!!!

Essentially, I did not let me starting point analysis become the end point analysis. Here, I shall share with you my selection criteria in general and what fascinates me the most about NVIDIA.

Hope you all enjoy reading about this Company as much as I do knowing it and learning about it:

As per Wikipedia, Nvidia Corporation is an American multinational technology company incorporated in Delaware and based in Santa Clara, California. It designs graphics processing units (GPUs) for the gaming and professional markets, as well as system on chip units for the mobile computing and automotive market. Its primary product, “GeForce”, is in direct competition with the GPUs of the “Radeon” brand by Advanced Micro Devices (AMD).

Do you know for NVIDIA, it took them more than a decade for the total number of developers to reach 1 million, but in less than 2 years, the number more than doubled to 2.3million developers. What a pace!!!

In Gaming world, NVIDIA happens to be a pioneer and holds the largest platform through GeForce of more than 200million gamers.

Eight of the world’s top 10 supercomputers use NVIDIA GPUs, InfiniBand networking, or both. NVIDIA powers 346 of the overall TOP 500 systems. Selene, NVIDIA’s own supercomputer, is ranked 5th in the world and is the fastest industrial supercomputer. And to top it all, the list of clients using NVIDIA devices, chips, clouds, gaming products just go on increasing every day.

Now let us look at how the numbers get played for the Company:

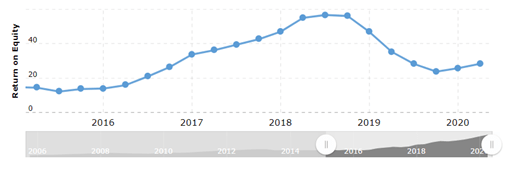

- Return on Equity (ROE): Nvidia has been consistently generating a high ROE and for the trailing 12 months, this ratio has been 29% and let’s have a look at this ratio for last 5 years:

Look at the average and the consistency on ROE. For majority of the time, it has hovered above 20% easily.

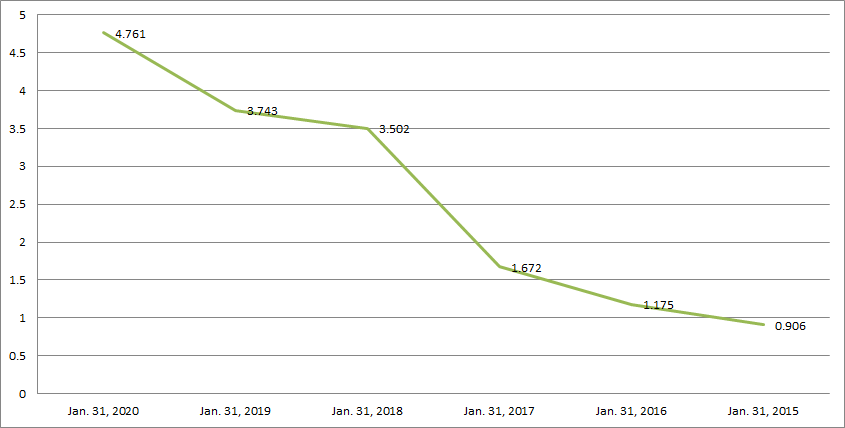

2. Long Term Debt to Equity of less than 1: Nvidia’s overall long term Debt to Equity ratio for the last 10 years has been a max. of 0.83 and a median of 0.22. Simply wow, isn’t this great Company generating enough cashflows/internal accruals to fund its growth!!!

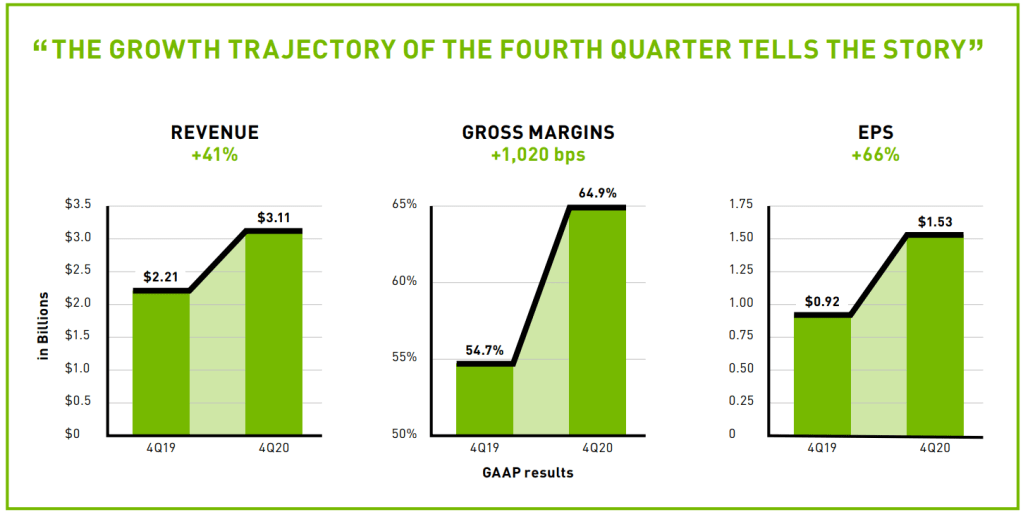

3. Revenue growth: Well, Company has been consistently generating a very high top line for last 5 years of over 15%. The Annual Report (2020) do mention the rising challenge as below:

As we entered the year, our outstanding growth was stopped in its tracks by the simultaneous headwinds of a collapsing cryptocurrency market, a pause in hyperscale spending, and a rapidly deteriorating trade environment with China. Despite being knocked back on our heels at the outset, we finished the year strong. Full-year revenue was $10.9 billion, down 7 percent. Gross margins expanded to 62 percent and GAAP earnings per share were $4.52, down 32 percent. We returned $390 million during the year to shareholders through quarterly cash dividends. The growth trajectory of the fourth quarter tells the story—with revenue of $3.11 billion, up 41 percent from a year ago.

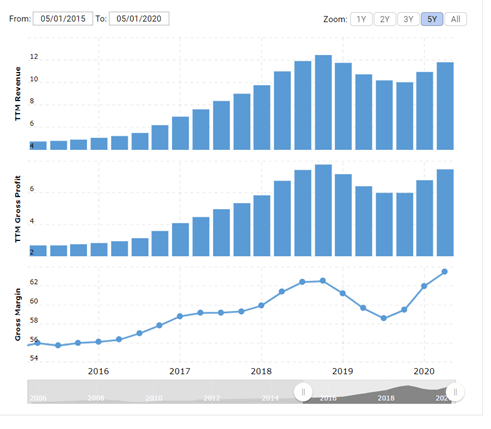

4. Growth Margins: Historically, Company has been generating decent Gross Margins of over 50% for last 5 years:

And to look at the margins for recent fiscal years,

Company also reports a decent net profit margins historically with recent figure being of over 28%.

5. Current Ratio: Here’s a look at the current assets & liabilities of the Company:

6. Sales growth Qtr. over Qtr. for the company has been over 10% which shows a good upward trend.

7. Operating Cash Flows: For me, the most important numbers to see the performance of the Company are the operating cash flows. As we call it in India, how much money finally comes in my pocket at the end of the day. Let’s have a look at the Operating cash flows for NVIDIA over last 5 years which have grown with a CAGR of 39%:

8. Free Cash flows: For last 5 years, let us have a look at the Free Cash flows:

The FCF have grown by CAGR of over 39% over last 5 years.

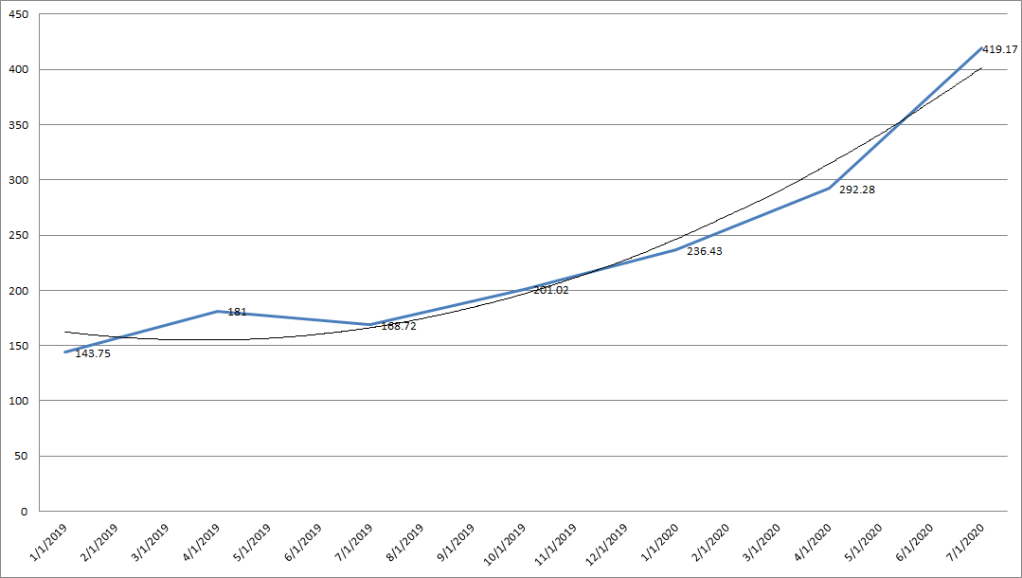

Valuation: I attempt to look at the following important metric that defines valuation for me but before that let’s look at the movement in Stock price:

The stock has rallied quite a lot in recent past. Let’s look at Price to Free Cash flow (for last 5 years):

Current PFCF Ratio is 27.58 while the average for last 5 years for the Company has been 16.21 and median has been 15.39. We see that the PFCF did touch 30 in 2017, but it has again started hovering at the same levels now. A clear case of Company being over-valued at the moment. But then valuation is a perspective and something very relative. If you believe the growth in the Company is going to be even better with most of the people sitting back home due to pandemic, then the over-valuation judgement today is just a statistic with no meaning!!!

Disclaimer: invested. Please ensure you do your research/analysis before making any decision.

Categories: Investor's Room